Banks, tech giants losing skilled workers to flexible fintechs

The exodus from Wall Street, the City of London and Silicon Valley has picked up speed during the pandemic, according to data from a workplace intelligence company.

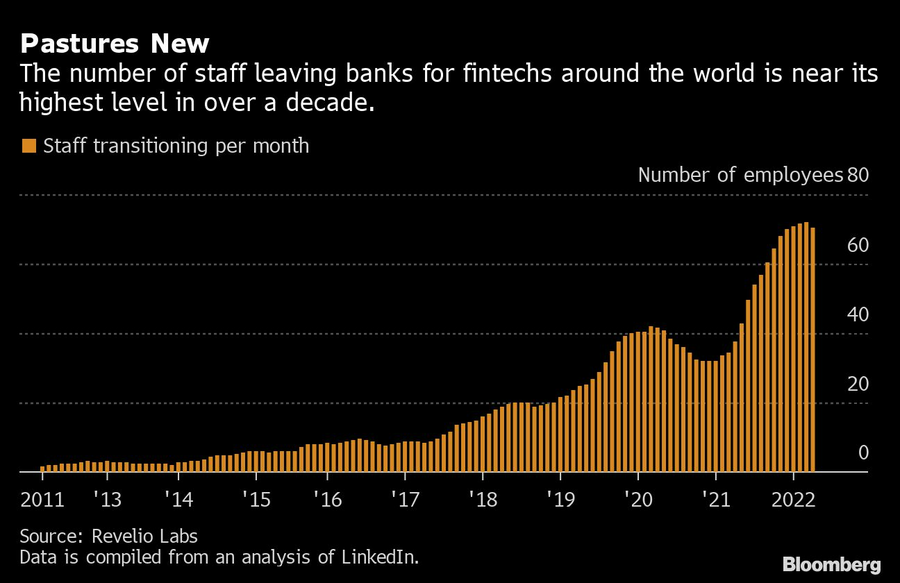

Staff at major banks and some of the world’s biggest tech giants are increasingly leaving for fintech startups, new analysis shows.

Bankers, engineers, data scientists and sales staff from Wall Street, the City of London and Silicon Valley are among those joining an exodus that picked up speed during the pandemic, according to data compiled by Revelio Labs, a workplace intelligence company.

Departures from traditional banks, such as Goldman Sachs Group Inc. and HSBC Holdings,. to fintech companies including Coinbase Global Inc. and Revolut Ltd. are up 75% since the start of the pandemic, Revelio said. Monthly job changes peaked at 72 in March this year — the highest figure since records began in 2011. Significant numbers of employees are also moving from tech firms like Amazon.com Inc. and Microsoft Corp.

Learn some top fintech companies in this article.

The growth in highly qualified staff switching to roles in new sectors comes as tight job markets allow many tech employees to change jobs, seeking higher salaries and more flexible routines.

Read more: How many jobs are available in tech: what jobs are in demand?

“People have stopped and reevaluated what’s important to them,” Lisa Simon, economist at Revelio, said in an interview. She cited a better work-life balance, improved pay and better career prospects as key drivers.

Goldman Sachs saw 37 staff move to Coinbase, the largest U.S.-based cryptocurrency exchange, from Jan. 2020 through April 2022. Another 21 Goldman staff joined corporate credit card start-up Brex Inc., while 18 went to SoFi Techologies, Inc., the fintech firm led by former Twitter Inc. executive Anthony Noto.

To be sure, the numbers of staff leaving for fintechs and startups are small in comparison to the overall numbers employed in major financial services firms or Silicon Valley tech giants. Goldman employs 45,100 people worldwide. A representative for the bank declined to comment.

Elsewhere, some 28 workers have gone from Morgan Stanley to Coinbase and 12 to Wise, which has almost 400 jobs available, according to a company spokeswoman. Some 38 HSBC employees have gone to Revolut and 21 to Monzo Bank. Challenger bank Monzo has also hired 32 former staff from Lloyds Banking Group and 27 from Barclays Plc.

Morgan Stanley and HSBC made no comment. In emailed statements, Barclays’ chief operating officer Mark Ashton-Rigby and a spokeswoman for Lloyds — which was recently ranked second in a LinkedIn list of the UK’s top 25 employers — each pointed to the importance their banks place on workplace culture.

“The number of people working in technology roles at Barclays has grown by more than 10% in the past two years which is testament to the compelling proposition we offer,” Ashton-Rigby said.

“There’s a war for talent,” said Christian Faes, co-founder of LendInvest and chair of the industry group Fintech Founders, citing high levels of regulation in traditional banking as well as “legacy processes, legacy people and technology.”

“We’re literally hiring people out of Facebook and Amazon, really high-tech engineers, and they don’t naturally gravitate toward banks with coding systems from the 1980s,” Faes said.

Coinbase alone has snagged 197 staff from Amazon, 97 from Alphabet Inc., the parent company of Google, 73 from Microsoft and 72 from Meta Platforms Inc., Revelio’s data show. Microsoft and Amazon declined to comment. A spokesman for Coinbase said the company is “pleased that so many employees from top banks and tech giants want to rebuild the future of the crypto economy.” Meta and Alphabet didn’t respond to requests for comment.

Despite the shift into fintech there are already signs the trend is easing off. Inflation is darkening the global economic outlook, and a major tech sell-off has put future funding rounds in doubt. Against that backdrop, the pace of staff movement from banking to fintech already appears to have slowed.

In that environment, some employees will choose stability over change. Crypto firms are looking especially risky: Coinbase’s market value has plummeted in the past six months, with the stock down more than 60% from its IPO price in April 2021.

That’s leading some to stick up for the key benefits of a mature, stress-tested financial sector.

“The basic story is we have customers and they don’t,” Zach Anderson, chief data and analytics officer at NatWest Group, said in an interview. “If you want to have an impact on 19 million customers in a substantive way, you go to a bank.”

Learn more about reprints and licensing for this article.