Jump to Winners | Jump to Methodology | View PDF

Americans are facing a growing need for guidance and support in their financial affairs and that trend doesn’t look like it’s going to end anytime soon.

Not only are people wealthier, but their financial situations are more complex relative to previous generations due to more retirees relying on savings, an increase in the range of products available, and the explosion in alternative investments.

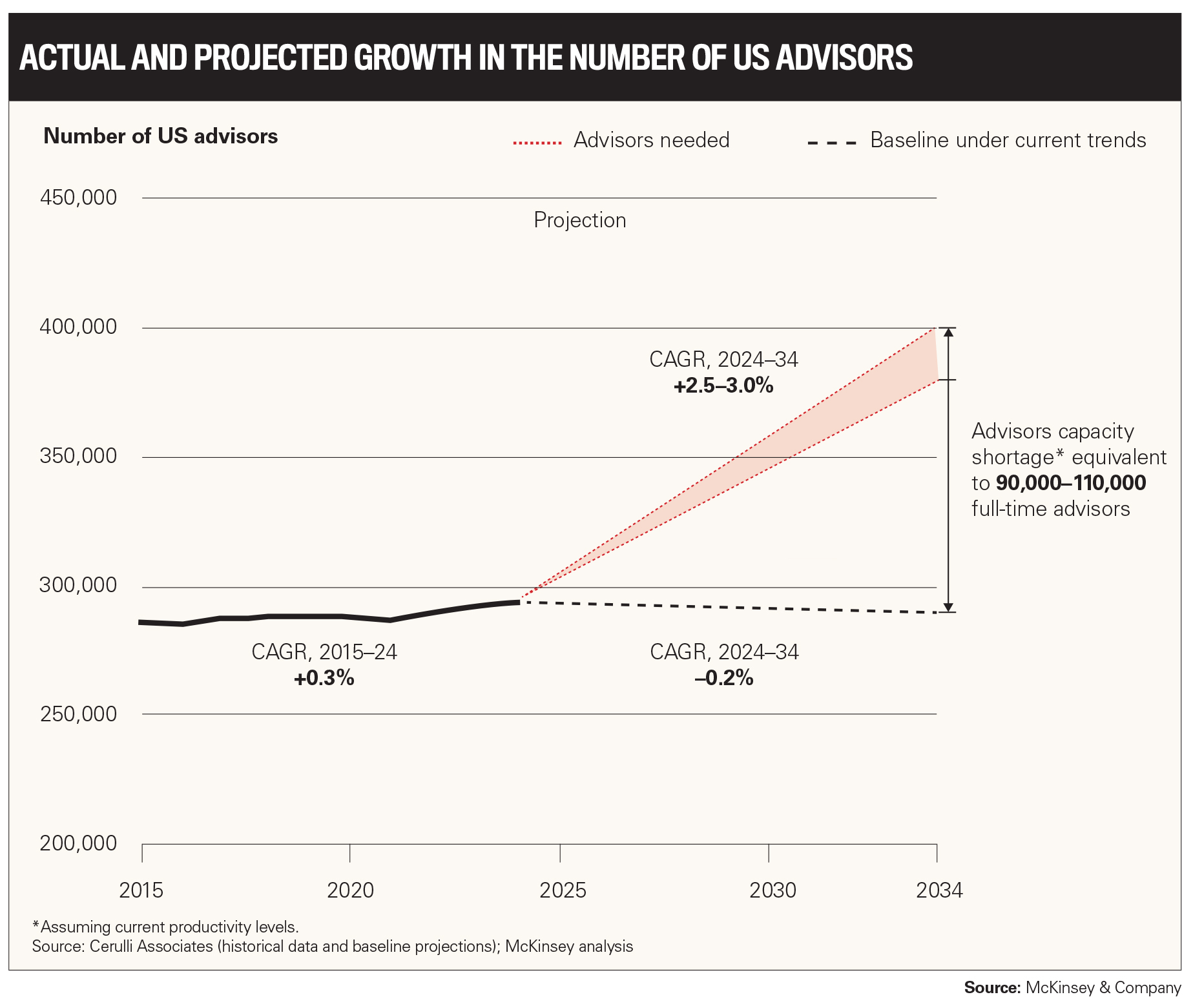

Consulting giant McKinsey & Company estimates that “by 2034, at current advisor productivity levels, the advisor workforce will decline to the point where the industry faces a shortage of roughly 100,000 advisors”.

McKinsey data also shows that the:

number of affluent households (with at least $500,000 in investable assets) will grow at four to five percent per year, compared with a 0.6 percent projected growth in overall population

share of investors seeking more holistic advice grew to 52 percent in 2023 from 29 percent in 2018

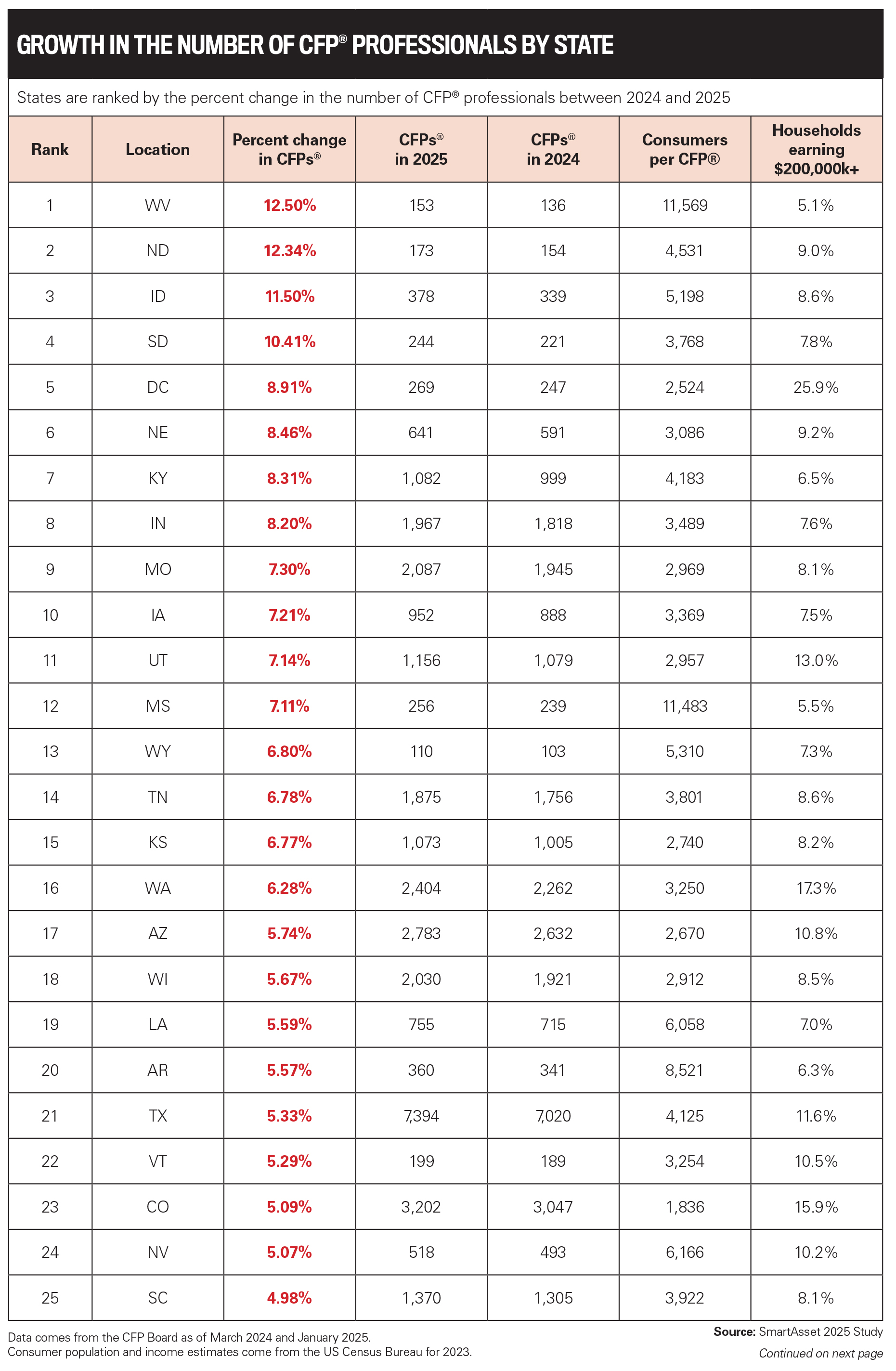

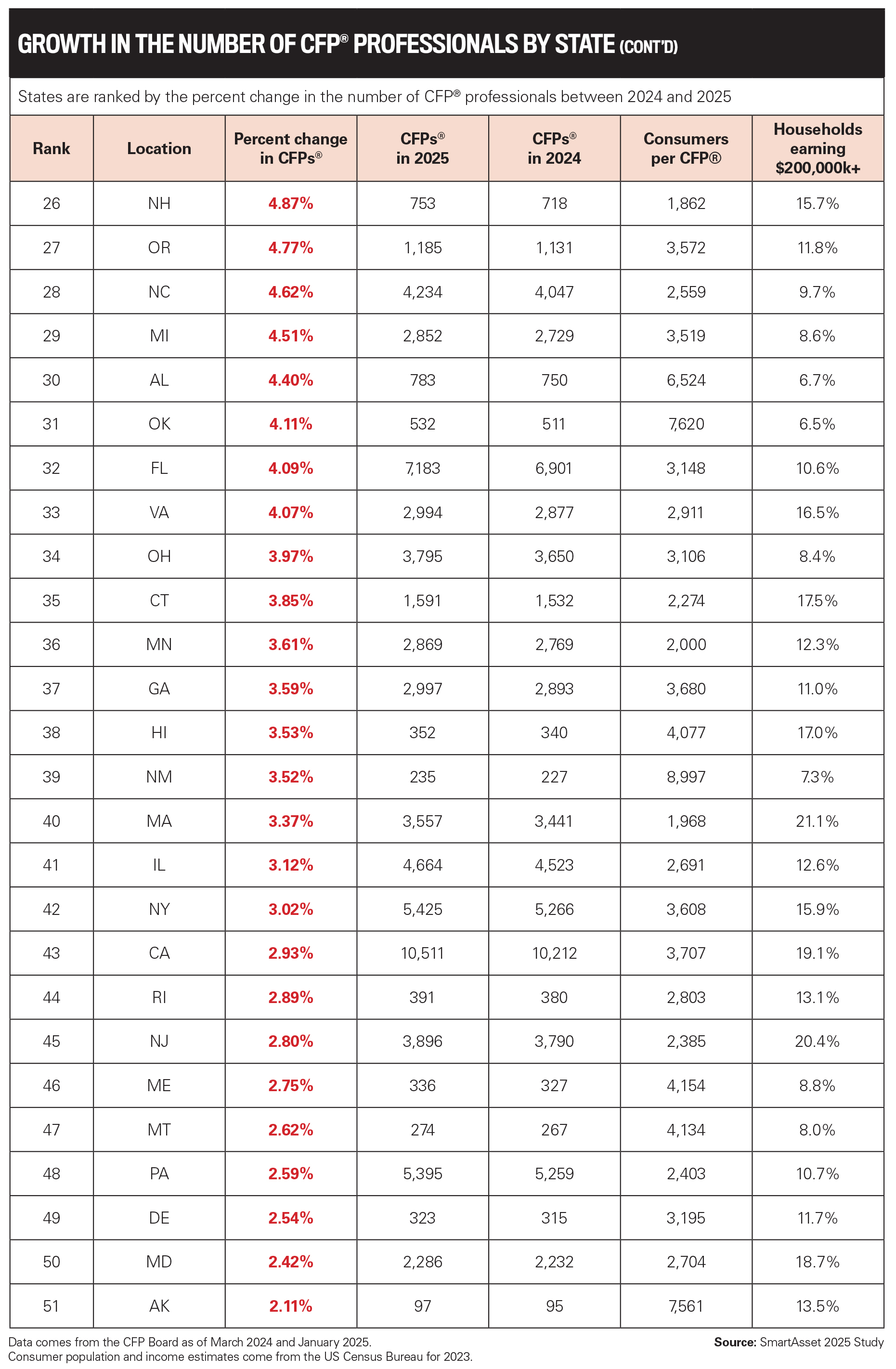

That is mirrored by an increase in the number of Certified Financial Planners (CFPs®) in 2024 by 6,500, bringing the total to 103,093 nationwide, according to a study published by client matchmaking service SmartAsset.

Some states are particular hotspots:

West Virginia had the highest rate of CFP growth. Relative to its 2024 population, the number of CFPs® increased by 12.5 percent in the past year.

California is home to over 10 percent of all CFPs®. There are 10,511 people with an active certification, making the ratio of consumers to CFPs® about 3,707 to 1.

Texas added the most CFPs® this past year, resulting in 374 more CFPs®.

The sharp demand for their services has pushed InvestmentNews’ 5-Star Financial Planners to stand out in a dynamic market by exemplifying excellence, integrity, and dedication in helping their clients. They were nominated and then benchmarked against others to determine the country’s best.

While the winners have varying skill sets, a commonality is the most successful financial planners specialize. They are serving a particular niche and have leveraged it to obtain a competitive edge.

Starting off at a public accounting firm, Robert Westley was tasked with advising high-net-worth (HNW) individuals and families on income taxes, which enabled him to develop a deep knowledge base.

“I was exposed to the whole ecosystem that surrounds wealthy families, some of the LLCs and trusts and foundations they set up,” says Westley. “My foundation in tax and accounting has really helped me, as a financial planner, to better understand the ecosystem and tax ramifications of certain transactions.”

What drew him to the HNW and ultra-HNW world is its labyrinthine nature. He relishes the challenge of delving into clients’ affairs.

“Their balance sheets are often more complex than some multinational corporations', with layers of trust and LLCs, and I find that fascinating. I really like the puzzle and complexity of it,” he says.

That’s also what attracted him to Northern Trust, as he intentionally sought out a firm in the space. Where Westley shines and is a difference maker is at the beginning with a new client. He adopts a forensic approach and leaves no stone unturned in understanding their complete picture.

He explains, “A lot of clients don’t necessarily have a road map of their financial situation. My first order of business is doing a deep discovery dive of combing through all their current investments, estate planning documents, income tax returns, and mapping it out where, on one or two sheets of paper, I capture all the assets.”

These can range from liquid and illiquid assets, private investments, life insurance, and tax-deferred accounts. Westley is also skilled at dealing with different generations of a family who stand to inherit. His role is not to dazzle them with figures but provide them with an understanding of the structure and rationale.

“They don’t necessarily know the dollar amount but understand what it means for them in the event of their parents passing,” he says. “It’s so once there is an event where it is fully transferred to them, they’re prepared and understand the complexity.”

Due to the level of detail and elaborate nature of his clients’ finances, Westley has a small core base. This enables him to develop close relationships and be an integral part of their support structure.

He says, “I’m really in the weeds and a lot of clients tell their spouse and children, ‘If anything ever happens to me, call Robert.’ When they have that confidence that there’s one person who really has the big picture, it helps them sleep better. For me, that’s a valuable part of the comprehensive financial planning process.”

Tech is part of the conversation for all leading financial planners, and while Westley is engaged, the nuanced nature of HNW work means he isn’t able to exploit it in the way some of his competitors are.

“We haven’t really found an off-the-shelf software that works, so we keep going back to Excel spreadsheets and have developed a lot of them that are customized,” he says. “There’s just so many different factors with trusts and LLCs, so there hasn’t been a perfect software solution where we’ve been able to just plug it in.”

Going forward, Westley has a subset of HNW clients – corporate executives – that he expects to need his services more. They are afforded large compensation packages and have tremendous wealth-building potential due to commonly being paid in stock options.

He says, “Their cash component is often very small compared to the overall compensation, which a lot of times is granted in equity. I help them make good decisions around that, so they’re left with a concentration, and then help manage and diversify that.”

Remaining free of conflict is Nichole Raftopoulos’s calling card.

After working at large firms, this leading financial planner realized that pushing products didn’t motivate her. Eager to remain focused on serving clients, she formed Nvest Financial. The firm has a client base across 26 states, is heavily focused on the New England seacoast and its retirement community. Its client base includes small business owners or those close to or have transitioned away from work.

Raftopoulos says, “We help people retire and we live with them during retirement. It’s not about checking boxes, it’s about changing lives.”

This approach ensures clients are listened to and supported. It’s normal for emails and cards offering gratitude to arrive at the office.

“The reality is we never take that for granted, and I’ll bring all those compliments back to the team and say, ‘Listen, remember, this is why we’re here,’” she adds.

What marks out the quality that Raftopoulos brings to the table is being able to communicate with the firm’s 900 clients. Naturally, she is not the lead planner for each case but works with her team, going through strategies, solving complex issues, and laying out scenarios.

This dedication means that each client receives the care and attention that Raftopoulos wants.

“When I’m working on cases with the advisor, we’re spending maybe half an hour on that, then they go back and deliver that beautiful experience, and I can work on the next advisor’s case,” she explains. “It leverages our skill set, and it continues to make sure our culture is growing and stays consistent with every single client experience.”

Having a single book of business is another of Raftopoulos’s initiatives. Every client is under the same umbrella.

“Any client of our firm is a client of all of ours. They might have a go-to person, but the clients know that I’m behind the scenes and I will have already met with them at some point. Every client feels that deep bench approach.”

Raftopoulos’s co-founder is husband George, but she has sole responsibility over the financial planning operation. They are focused on remaining in control despite the trend of independents being bought out and joining big RIAs. The plan for Nvest Financial is to keep growing, and the firm is also looking at acquisitions but only if it’s a cultural fit and value match.

“We get offers nonstop about being bought and becoming part of something bigger, but we really have that independent focus,” says Raftopoulos. “We really want to focus on our culture and what we do for our clients, and we don’t see that it fits a lot of times when you’re giving someone else control of your firm.”

Another standout performer who entered the industry by a circuitous route, Eileen Allgrove has made a name in estate planning and trusts. The law school graduate had an initial edge armed with deep legal knowledge.

She says, “In some ways, that initial lack of a finance background helped me learn how it felt to be intimidated by something out of my comfort zone, and then taking steps to acquire knowledge that I would apply. This is the same track I provide to my clients.”

Each case is part of the changing landscape that Allgrove faces, with families having different goals. To be able to deliver, she has to be an effective communicator.

She explains, “During my time as a trust officer, I witnessed both good and poor family communication. Estate planning, particularly for those with significant wealth, is usually centered around tax savings, which requires mechanisms of control and secrecy.”

Part of her role is to prevent clients from adopting bad money habits, due to the feeling that someone else is controlling their wealth. This extends across the generations.

“By fostering communication, education, and understanding with the entire family, it is more likely that there will be a successful transition of wealth,” says Allgrove.

When working with families that don’t have taxable wealth, she collaborates and meets all her clients as a unit annually.

“That way, when a health crisis or sudden death happens, everyone is better able to communicate and trust each other. There are some situations where family members aren’t ready for the full picture and those are situations where we try to have more educational focused meetings, to try to set the basics to prepare them for larger conversations in the future,” she explains.

Allgrove is a believer in not inundating clients with info and won’t show them 60-page reports. Her approach builds the foundation and expands upon it. To do this, she has deployed various tech tools, such as MoneyGuide, Holistiplan, and NaviPlan, but uses eMoney more frequently.

She says, “I try to present the information in sections, meaning we start with net worth or balance sheet, and then move on to other topics as we proceed with the planning process.”

Providing clients with an improved understanding of their financial picture and furnishing them with greater confidence in their relationship with money is a successful result for Allgrove.

“I think some planners can be too focused on what makes sense from a tax, risk tolerance, or result approach,” she says. “I like to focus on where we are, what the goal is, and work collaboratively to make changes – big or small – to get there.”

Shaping the firm in his own image has enabled Scott Van Den Berg to exploit his range of skills.

The Austin, TX-based organization, which is backed by a team of seasoned CFPs and CFAs with decades of experience, has a trio of specialties:

retirement planning for business owners and individuals

tax-efficient income strategies for retirees

real estate investment and strategic transactions

“We don’t just create a one-time plan – we stress-test it against multiple what-if scenarios. We go beyond the numbers to help clients navigate life’s financial decisions with clarity and confidence,” says Van Den Berg.

It’s a highly customized approach, analyzing every detail of a client’s financial life, including their equity and fixed income investments, rental properties, and business interests.

A notable talent of Van Den Berg’s is assisting business owners in securing research and development tax credits and accelerating depreciation through cost segregation. This maximizes financial efficiency while ensuring full compliance with tax regulations.

He works closely with CPAs and tax professionals to analyze eligible activities, helping to ensure clients capture the full benefits of innovation-driven expenses such as product development, process improvements, or software advancements.

“My role is to educate, help uncover qualifying expenses, and integrate the savings into a broader financial strategy. For cost segregation and accelerated depreciation, I assess a client’s real estate holdings to identify opportunities to reclassify assets into shorter depreciation schedules,” he says.

“Working with CPAs that specialize in this area, we help break down a property into its components, such as electrical systems, flooring, and HVAC. This helps clients accelerate depreciation, freeing up capital that can be reinvested or used to offset taxable income.”

In one particular case that Van Den Berg calls a “game changer,” he advised a small business owner to transition from a SEP IRA to a cash balance pension plan with a 401 (k).

“The key lies in understanding the limitations of SEP IRAs. While simple, they cap annual contributions at a much lower level than a cash balance plan, which allows for significantly higher tax-deferred savings,” he explains. “For businesses with one to five employees, a defined benefit plan can be a great solution, whereas for companies with five to 30 employees, a cash balance plan often provides greater flexibility and efficiency.”

After assessing the cash flow to confirm the business could sustain higher contributions, Van Den Berg worked with actuaries and third-party administrators to optimize tax savings while keeping costs manageable.

He says, “In most cases, business owners can save significantly more than they could with a SEP IRA, while also enhancing employee retention and benefits. These custom pension strategies help business owners build wealth faster, reduce tax burdens, and create financial security – all while supporting their employees.”

Alongside his team, Van Den Berg uses leading software, such as eMoney, Holistaplan, Horsesmouth, HiddenLevers, S&P Capital IQ, and Bloomberg, for deep analysis and data-driven strategies.

“By integrating cutting-edge technology with our decades of expertise, we provide clients with clear, strategic, and informed financial guidance, so they remain on track to achieve their financial goals with confidence,” he explains.

Outside of their technical skill set, the 5-Star Financial Planners have to be empathetic and intuitive. They understand their clients and connect on a human level to address concerns, whether due to market volatility, life changes, or economic uncertainty.

Below, the winners explain how they’ve navigated and become adept at the softer side of the business.

Robert Westley: “It’s a learning process. You have to be there for clients when they go through life events. I’ve had clients that lost a child, which is God-awful. The interpersonal skills develop over time as you go through these situations. It’s about making yourself available as sometimes they just want to talk. You don’t necessarily have to give an answer, but it’s reassuring for clients to know they can pick up the phone and have a conversation with you.”

Eileen Allgrove: “I am a working mother with young children, so stress is a constant. I have been in the industry for 25+ years and experienced the tech bubble, the the 2008 crisis, and the COVID-19. What I have learned is to stick with your plan, be positive if things are not going in the expected direction, and be resilient and flexible. And if you see someone struggling, be willing to listen and provide support and encouragement. Sometimes listening and allowing someone to get something off their chest is all that is needed.”

Scott Van Den Berg: “Financial planning isn’t just about numbers – it’s about people, their goals, and the emotions tied to their wealth. One of the most important ways we do this is by reminding clients of their long-term goals and helping ensure their financial strategies remain aligned, no matter the market cycle. Clients need to know they are heard and understood. I always give clients my personal cellphone so they can reach me when needed. As a firm, we make it a priority to return every client call the same day – no one should feel ignored or left in the dark.”

Senior Vice President, Private Wealth Manager

Integrated Equity Management

InvestmentNews conducted a nationwide survey between November 18 and December 13 to recognize outstanding financial planners in America. The survey sought nominations for financial professionals who exemplify excellence, integrity, and dedication in helping clients achieve their financial goals. Participants were asked to provide detailed information on nominees, including professional credentials, areas of expertise, and significant achievements.

Nominations required confirmation from the nominee’s compliance team to ensure authenticity and adherence to ethical standards.

The IN team conducted an objective evaluation of each entry, assessing the detailed information provided. This evaluation also involved benchmarking against other submissions to determine the winners.