While Janus Henderson’s AAA CLO ETF recently surpassed $20 billion in assets under management, other fund managers and financial advisors say that CLO ETFs with exposure to lower debt ratings are becoming preferred targets for investors moving forward.

“In the institutional world, a lot of banks and insurance companies may only invest in AAA tranches because they are heavily regulated entities – they have capital requirements and the ratings dictate that,” said Bill Sokol, vice president and director or product management at VanEck. “But if you're a typical investor with a core fixed income portfolio, you're not constrained to AAAs. We think the best way to build a stronger core portfolio is a broad investment-grade approach, for the higher yield and better total return opportunity.”

VanEck’s CLO ETF, which holds $911 million in total net assets, was launched in 2022 and invests primarily in investment-grade-rated tranches of collateralized loan obligations (CLOs). VanEck’s other AA-BB CLO ETF launched in September 2024 and now has $66 million in net assets.

In January, BlackRock launched its iShares BBB-B CLO Active ETF, another example of an asset manager tapping into debt tranches below the top-tiered AAA.

Shortly after the first CLO ETFs launched in 2020, their total assets were around $120 million, but that total has since ballooned to more than $25 billion, said Kirsten Chang, senior industry analyst at VettaFi.

“Lower down the credit-quality spectrum, the expense ratios are higher, because the risk is higher. But I do think that we are going to see more and more of these BBB to B ETFs, because the AAA space is just getting too crowded,” Chang said. “You can only go so far down the spectrum though, because once you get below BB or so, you’re running out of liquidity.”

Before CLO ETFs emerged in 2020, CLOs were mostly limited to institutional investors with at least $100 million in assets necessary to qualify for them. ETFs not only provide new opportunities for retail investors but also carry increased diversification, with as many as 150 to 300 loans bundled into one CLO ETF, Sokol said.

“CLOs have just been a very good place to earn very attractive income and avoid the rate volatility you're getting in really any area of fixed income the last few years. It's really been one of the only that performed well,” Sokol said. “Right now, yields are still high in the short end. These are floating-rate instruments. You still do get very high yield. Even though the Fed has cut rates a few times, the policy rates are still quite high.”

CLOs are structured around corporate credit, primarily bank loans to major corporations. The structure is often mistakenly conflated with CDOs (collateralized debt obligations) – a different class of securitized assets whose defaults were a main trigger to the 2008 global financial crisis.

“There's still a very real educational barrier to break through when it comes to CLOs, because people often conflate CLOs with CDOs, which were the true culprits back then,” Chang said. “You have large corporations backing these [CLO] loan payments with much higher quality credit ratings, while some CDOs relied on consumers to cover their mortgage payments, not corporations. Obviously, those struggled as those subprime mortgage payments became unfeasible.”

CLOs debuted in the 1990s and have never experienced a AAA default. Data from VanEck show that of the 783 BBB-rated CLOs issued before the 2008 financial crisis, just nine (1.1 percent) defaulted, while no BBB or higher rated ones have defaulted since 2008.

“CLOs have been around since the ’90s. So they went through the financial crisis along with those CDOs and securitized subprime mortgages – and CLOs did very well,” Sokol said.

Among the 16 CLO ETFs in the US, PGIM’s AAA fund has $2.4 billion in net assets, making it the second-largest, behind Janus Henderson’s JAAA, which was issued in 2020. In December 2024, BondBloxx and Virtus launched the industry’s first two private credit CLO ETFs.

Investment managers are generally optimistic about the direction of CLO ETFs and anticipate minimal liquidity issues. However, Matt Malone, head of investment management at Opto Investments, cautions that corporations whose borrowed money is tied to CLOs could have their bottom lines affected by new tariff policies introduced by the Trump administration.

“If you look at bigger internationally exposed businesses, which are probably the type of businesses that are getting bank loans or high yield bonds, I think those businesses are going to be more impacted by tariffs, versus private companies, which tend to be domestically focused,” Malone said. “If your [CLO] is exposed to a lot of larger companies that are generally revenue producing inputs internationally, those companies are more impacted. Their costs are potentially going to go up and their EBITDA (earnings before interest, taxes, depreciation, and amortization) margin is going to be squeezed. That may cause some credit coverage issues in those types of companies.”

LifeMark Securities has faced scrutiny in the past for its sales of GWG L bonds.

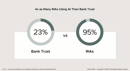

New data from F2 Strategy shows 95% of RIAs are using AI - four times the adoption rate of banks. Trust companies account for 90% of firms not using AI, raising alarms about their ability to stay competitive.

The ex-registered broker facilitated a series of transactions, including nine trades totaling nearly $130,000 and eight withdrawals amounting to $85,000, for a fourteen-month period after the client's death.

The wealth tech giant is offering advisors a natural, intuitive way to use AI through its new business intelligence and insights engine features.

Sometimes letting clients lead conversations, rather than having all the answers, can be the most powerful trust-builder.

How intelliflo aims to solve advisors' top tech headaches—without sacrificing the personal touch clients crave

From direct lending to asset-based finance to commercial real estate debt.