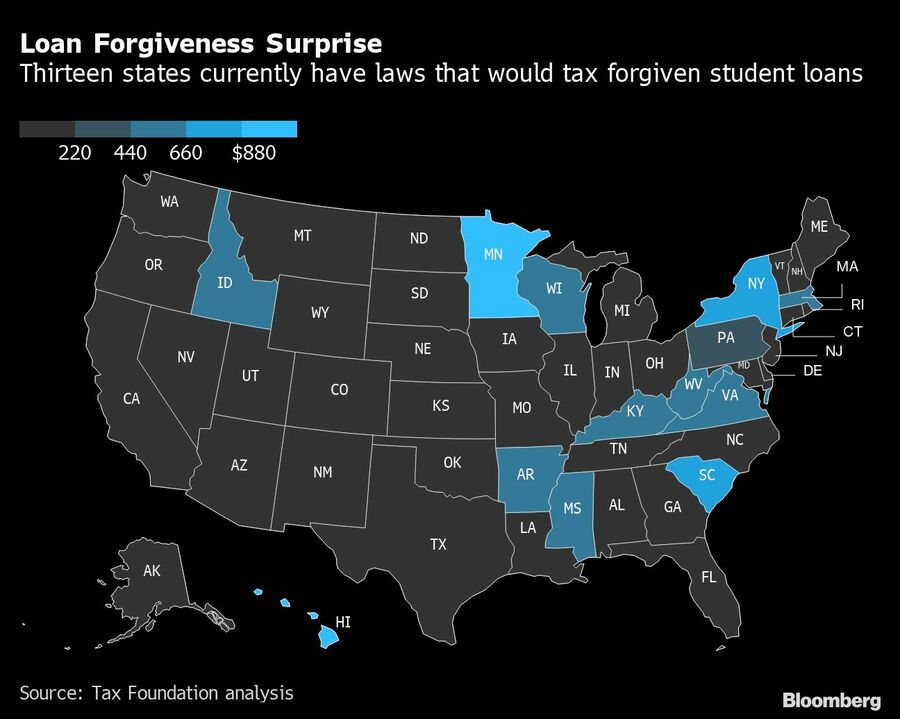

Residents of New York, Virginia and 11 other states could end up with a surprise tax hit of hundreds of dollars next year on forgiven student loans.

President Joe Biden’s announcement that the government would forgive some student debt for individuals earning less than $125,000 was welcome news to many carrying large loan balances. But 13 states have laws that treat this forgiven debt as income, meaning that it’s subject to state levies on earnings.

That means that taxpayers in those states who have $10,000 in debt forgiven could end up owing a few hundred extra dollars -- or in Hawaii more than $1,000 -- on their state tax returns next April.

Student borrowers who received a Pell Grant as an undergraduate, which the White House estimates is about 60% of borrowers, can get up to $20,000 in loans forgiven. Individuals with the full $20,000 cancelled would pay double the tax amounts.

The federal tax code also generally treats forgiven debt as income, but in 2021, Congress included in the American Rescue Plan a measure that would temporarily exempt canceled student debt from taxation.

It’s possible that some of the 13 states where the laws would tax these forgiven student loans will revise their rules before the taxes are due next spring. Depending on the state, that could come in the form of an administrative change from the governor or state tax department, or may require the state legislature to pass a new law.

Jared Walczak, a vice president at the Tax Foundation focusing on tax policy, calculated the maximum tax hit for $10,000 in forgiven loans in various states. His figures are based on the highest tax rate filers who qualify for loan forgiveness are likely to pay in their state. His tabulations found that residents of Pennsylvania are likely to pay the lowest amount, with Hawaiians paying the most.

| State | Maximum Likely Tax Liability |

|---|---|

| Arkansas | $550 |

| Hawaii | $1,100 |

| Idaho | $600 |

| Kentucky | $500 |

| Massachusetts | $500 |

| Minnesota | $985 |

| Mississippi | $500 |

| New York | $685 |

| Pennsylvania | $307 |

| South Carolina | $700 |

| Virginia | $575 |

| West Virginia | $650 |

| Wisconsin | $530 |

Walczak said that states will need to act with “some urgency” if they want to change how their tax laws treat student loans in light of Biden’s changes. He added that it isn’t likely to matter whether the state is led by Republicans or Democrats. Since the change has already been made at the federal level, there will be some pressure on states to reduce tax burdens for their residents, he said.

Integrated Partners is adding a mother-son tandem to its network in Missouri as Kestra onboards a father-son advisor duo from UBS.

Futures indicate stocks will build on Tuesday's rally.

Cost of living still tops concerns about negative impacts on personal finances

Financial advisors remain vital allies even as DIY investing grows

A trade deal would mean significant cut in tariffs but 'it wont be zero'.

RIAs face rising regulatory pressure in 2025. Forward-looking firms are responding with embedded technology, not more paperwork.

As inheritances are set to reshape client portfolios and next-gen heirs demand digital-first experiences, firms are retooling their wealth tech stacks and succession models in real time.