Tracey Warson left New York on a mission.

The head of Citigroup Inc.’s private bank in North America moved cross-country to San Francisco last year to court the Bay Area’s growing pool of wealthy entrepreneurs and newly minted tech millionaires.

“There’s a different energy here,” Ms. Warson said. “In New York you feel the markets energy, here you can feel the technology and the innovation.”

A lot of her competitors also have picked up on that vibe. Bank of America Corp., Morgan Stanley, Deutsche Bank and JPMorgan Chase & Co. are among the Wall Street firms beefing up their wealth management teams in Northern California, adding staff and resources to the fast-growing market.

But even as they expand their presence in the Bay Area, big banks often find themselves as outsiders. In a town that places such high value on disruption and thinking differently, Wall Street is still considered “old guard,” according to venture capitalist Arjun Sethi. The culture clash between entrepreneurs and bankers is evident even in their clothing, he said.

“Here in the Valley, if you’re meeting someone with a suit and tie, you feel like they’re selling you snake oil,” said Mr. Sethi, who favors jeans and hoodies.

Low-key wardrobes notwithstanding, the region is flush with cash. In the 12 months through September, more than half of the $122 billion of venture capital investments made in the U.S. went to Bay Area and Silicon Valley firms, according to PricewaterhouseCoopers.

Then there are the IPOs.

Fourteen San Francisco-area companies that began trading publicly last year have raised more than $15 billion, led by Uber Inc.’s $8.1 billion and Lyft Inc.’s $2.3 billion, according to data compiled by Bloomberg. Expand that to include the 16 other Bay Area firms that have gone public and the amount jumps to more than $20 billion.

The world’s largest banks have latched on to the explosion of wealth during the decade-long bull market. Wealth management units of nine of the biggest firms are set to surpass $100 billion globally in combined revenue for a third straight year, contributing about one-fifth of the banks’ total revenue.

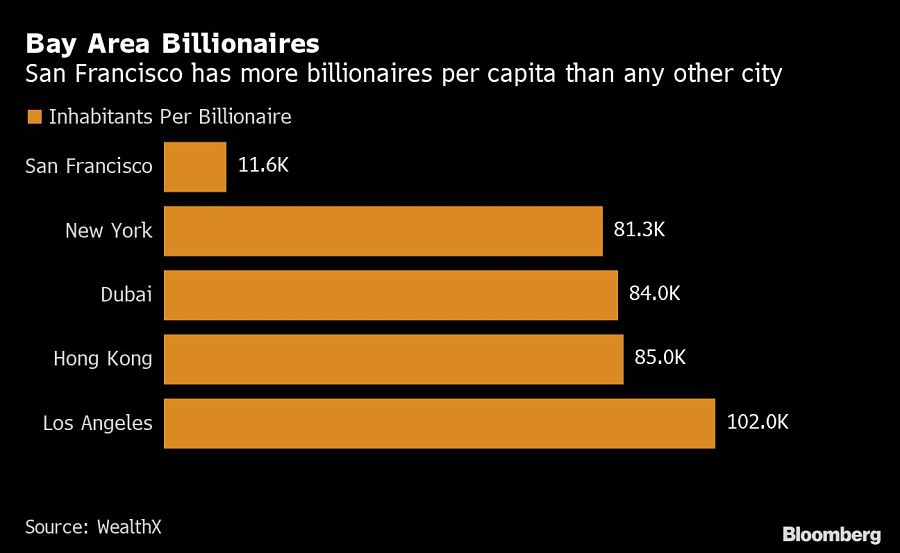

Even with the disappointing post-IPO performances of some Bay Area companies, the newfound liquidity has minted thousands of millionaires and more than a few billionaires. The flood of new money has made the area one of the world’s hottest wealth markets, especially given the number of potential clients who lack longstanding relationships with financial firms.

“Anybody who’s in the business knows that this is where wealth is being created,” said Christine Leong, head of JPMorgan’s Northern California wealth management division, which oversees $15 billion in the Bay Area. “We want to make sure we are well-positioned and helping advise these entrepreneurs early on.”

In mining these riches, Wall Street banks are up against dozens of boutique firms.

Some are homegrown, such as San Francisco-based Hall Capital Partners. Others were started by advisers who broke away from wirehouses.

Iconiq Capital, for example, was started by former Goldman Sachs banker Divesh Makan, whose early clients included Facebook Inc.’s Mark Zuckerberg and Twitter Inc.’s Jack Dorsey. As of July, the firm managed about $14 billion in assets and advised on an additional $18.8 billion.

When company founders ask for wealth management advice, Mr. Sethi said he typically sends them to registered investment advisers.

“They’re upstarts, so there’s familiarity with that versus, ‘Hey we’re this big bank, we know everything and we are going to tell you what to do,’” he said.

Investment bankers

It takes creativity for private bankers to get in front of potential clients. Forming relationships early with executives at unicorns-to-be is important and often requires the help of investment bankers. Introductions have to be made quickly before “they’re flooded with phone calls, and they’re not always going to look at the big bank,” said Michael Rogers, Deutsche Bank’s West Coast head of wealth management.

About a fifth of his clients come from investment bankers who are working with startups, Mr. Rogers said.

Deutsche Bank primarily manages money for those with fortunes of $30 million or more, so it’s mostly focused on getting in front of C-suite executives. But other groups with smaller minimums will tap lower-level employees as potential clients.

JPMorgan advisers have held presentations over lunches and dinners with tech employees of varying levels, Ms. Leong said. It doesn’t always generate immediate business, but there’s the possibility that someone in the room might have their own startup one day, she said.

Basic networking

Citi’s Warson said her team has coordinated dinners with private bank and investment bank clients to create a direct line between existing and potential wealth management customers. It’s a way of saying, “We’re here for you tech entrepreneurs when you’re ready,” she said.

Banks also use basic tactics such as sending LinkedIn messages to people like Han Jin, the 31-year-old founder and chief executive of Lucid, a 3-D photo startup.

Mr. Jin said he has been approached by Charles Schwab Corp. and Morgan Stanley, among others, about their wealth management services. After meeting with them and another family office, he decided to just use phone apps for now.

“It feels more in control — at least for Silicon Valley entrepreneurs who are very techy,” Mr. Jin said, adding that he has four or five apps that he uses for managing his money.

Balance sheets

Mr. Jin said that as he gets wealthier — he’s worth a couple of million dollars now — he’ll likely turn to a wealth manager for help, but will probably work with a smaller boutique firm first.

“The individual service is much better,” he said.

Big banks point to their value as lenders as a way of differentiating themselves from boutiques. With huge balance sheets, they can make lines of credit available to wealth clients and unicorn founders, who sometimes have little liquidity until their firms go public.

“In many cases, they don’t have a lot of income because they’re not paying themselves a lot,” said Dan Schrauth, a wealth adviser at JPMorgan. “But they have a lot of equity and the company is really exciting and going places, so maybe we could help them look at creative financing, get a mortgage or unlock other liquidity.”

While it can be complicated at times, such lending is a crucial part of Citi’s private bank offerings, Ms. Warson said.

Offering liquidity

“We can do very interesting, unique structures,” she said. “Depending on the profile of the client, we can find ways to get them liquidity.”

These deals can be highly profitable for the banks, but do carry risk — especially as sky-high private-market valuations are being questioned and more IPOs flop.

Former WeWork CEO Adam Neumann became a poster boy for such risks. The co-founder of the office-sharing firm borrowed hundreds of millions of dollars from JPMorgan, UBS Group AG and Credit Suisse Group against his private shares in the firm.

WeWork’s plans for an IPO were scrapped late last year after investors balked at the company’s proposed valuation and unflattering media reports about its corporate culture. Neumann was forced to step down as chairman and CEO, but still walked away a billionaire.

Driven by robust transaction activity amid market turbulence and increased focus on billion-dollar plus targets, Echelon Partners expects another all-time high in 2025.

The looming threat of federal funding cuts to state and local governments has lawmakers weighing a levy that was phased out in 1981.

The fintech firms' new tools and integrations address pain points in overseeing investment lineups, account monitoring, and more.

Canadian stocks are on a roll in 2025 as the country prepares to name a new Prime Minister.

Carson is expanding one of its relationships in Florida while Lido Advisors adds an $870 million practice in Silicon Valley.

RIAs face rising regulatory pressure in 2025. Forward-looking firms are responding with embedded technology, not more paperwork.

As inheritances are set to reshape client portfolios and next-gen heirs demand digital-first experiences, firms are retooling their wealth tech stacks and succession models in real time.